How Much Higher Will Tree Prices Rise? (June 2016)

Landscape Tree Market Outlook For Florida and the Southeast 2016 – 2019

By Timothee Sallin – President, Cherry Lake Tree Farm

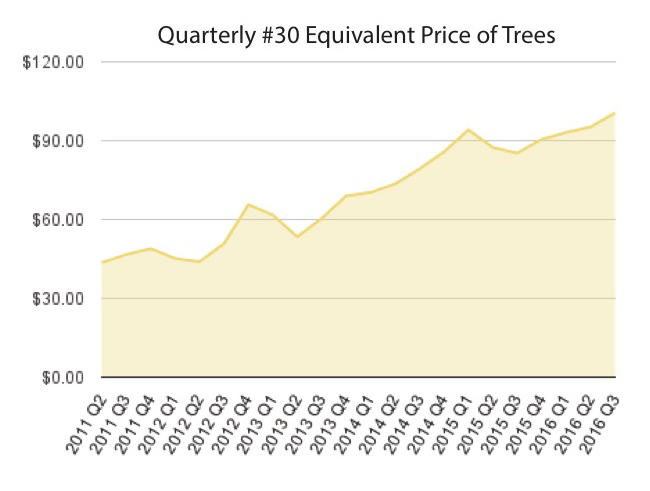

As we move into the third quarter of 2016, we can look back on 23 quarters of price escalations in the landscape tree market. Prices have increased by over 100% since they bottomed out in the third quarter of 2010. This sustained rally in prices has us asking a few questions: How much higher will prices rise? Will prices return to pre-shortage levels? What is the new normal?

Economic fundamentals of supply and demand in the tree industry indicate that the market for trees will continue to tighten over the next 24-36 months and prices will increase at least 30% before stabilizing between $130-$140 per 30 gallon equivalent. To support this forecast, I will discuss trends in supply and demand, housing starts, inflation, cost of production inputs, and the expectations of return on capital in the ornamental tree industry.

Supply and Demand

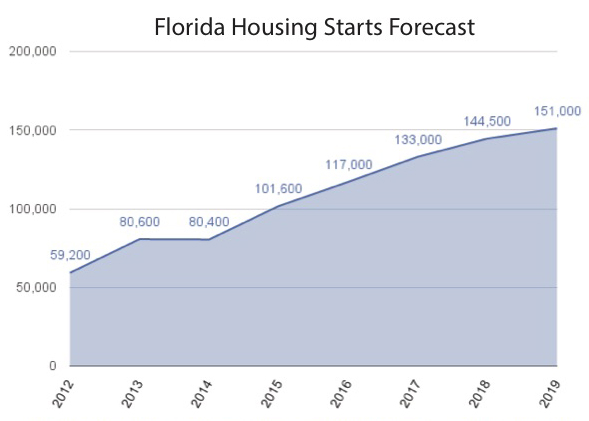

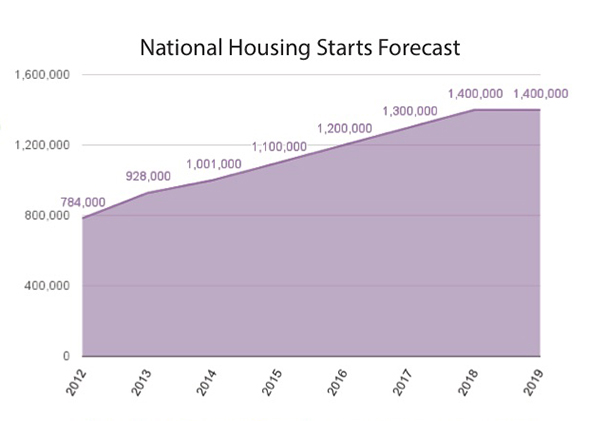

The major swings in tree prices over the past 10 years illustrate how sensitive prices are to changes in supply and demand. The precipitous fall in prices between 2007 and 2010 was the result of a substantial increase in supply, coinciding with a massive reduction in demand during the Great Recession. Since 2011, prices have been increasing consistently as housing markets recover and supply struggles to catch up. How much higher will prices rise? To answer this, we must consider the outlook for supply and demand. If demand grows at a faster rate than supply, prices will continue to rise. Alternatively, if supply increases at a higher rate than demand, prices will fall. We can forecast demand by looking at housing start forecasts and real estate market trends. In Florida, housing starts increased 26% year over year in 2015 and are projected to increase by 15% in 2016 and 14% in 2017. Nationally, the picture is much the same, with housing starts increasing 18% year over year in 2015 and projected to increase by 8% in 2016 and 10% in 2017. From these statistics, we can anticipate demand for trees to continue to grow at a rate of at least 10% per year over the next 24-36 months. In order for prices to come down, supply would need to grow over 10% per year in this period.What is a 30 Gallon Equivalent?

The 30 gallon equivalent is a size-weighted index in which each item influences the index in proportion to its size relative to the 30 gallon. A typical 30 gallon tree is 10′ tall, 2″ caliper, and about three years old. Larger sizes take longer to produce and, therefore, have higher 30 gallon equivalent value. This index makes it possible to track price and volume of tree inventories as an aggregate including ball and burlap and container inventories.

“Since 2011, prices have been increasing consistently as housing markets recover and supply struggles to catch up.”

UCF Institute for Economic Competitiveness Florida Metro Forecast

UCF Institute for Economic Competitiveness Florida Metro Forecast

Limiting Factors to the Growth of Supply

My expectation is that supply will grow at a rate of 3-5% per year over the next 24-36 months. This is based on a consideration of the limiting factors to the growth of supply. These limiting factors are space and infrastructure availability, starter kit availability, capital requirements, and grow time. Space and infrastructure availability is the total amount of unused nursery capacity available for planting. In order for supply to increase, there must be available infrastructure for expansion, including land, irrigation, and holding systems. Much of the industry’s production capacity was destroyed during the Great Recession, with large amounts of acreage being abandoned or converted to other uses. While there was excess capacity available at the start of the recovery, most of this has already been filled. In order for supply to continue to grow and to keep up with demand, new infrastructure will need to be created which requires both capital and time.

“Much of the industry’s production capacity was destroyed during the Great Recession, with large amounts of acreage being abandoned or converted to other uses.”

Starter kit availability is another constraint to the growth of tree inventory. Starter kits are 1 or 3 gallon trees purchased by growers to start their crops. The great recession significantly reduced the supply and production capacity of this sector as well. As a result, there has been a persistent shortage of starter kit materials since the beginning of the recovery. Without an adequate supply of starter kits, it is not possible for the industry to increase the inventory of finished trees quickly enough to keep up with housing growth.

Capital requirements are another limiting factor. As we have seen, significant increases in supply will require new land and infrastructure for growing trees. This requires new capital. Most growers’ working capital has been critically reduced as result of the great recession, and they are limited in their ability to finance major expansions. As I will discuss in more detail below, it is unlikely that new capital will be attracted to this industry in sufficient amounts to substantially impact supply over the next 24-36 months.

Finally, grow time, is nature’s ultimate constraint to the growth of supply. Even if all the other enabling factors were in place – infrastructure, starter kits and capital – trees still require 4-5 years to mature to code minimum 3” and 4” caliper specifications. The supply of trees for 2017, 2018 and 2019 is based on the planting of new inventory in 2013, 2014 and 2015. All indications are that growth in supply will not outpace demand and we can expect a continued tightening in the market over the next 24-36 months.

Real Prices v. Nominal Prices

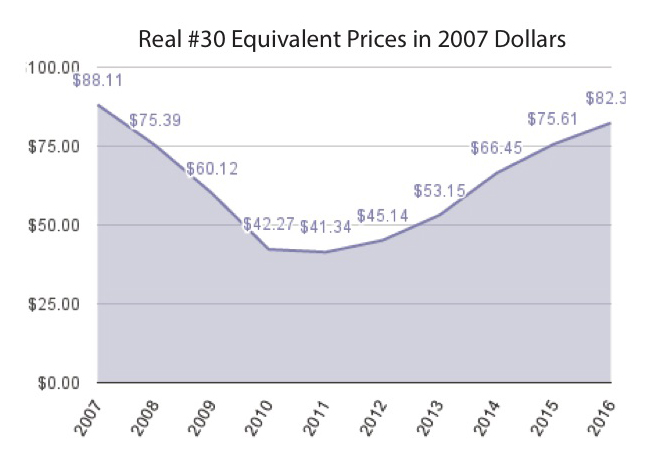

The price escalations over the past 6 years have been significant – over 100% since 2010. In large part, these increases have been a recovery of prices previously lost during the great recession. Today, the nominal price (not adjusted for inflation) is only slightly higher than it was in 2007. When we adjust prices for inflation, today’s prices are, in fact, 7% lower than they were in 2007. 3

This chart provides perspective on the recent price escalation. In nominal terms, the price increases can seem dramatic to buyers and sellers, however, a closer reading of the data reveals the industry has not yet regained all of the ground lost during the Great Recession.

“Today’s prices are, in fact, 7% lower than they were in 2007.

Cost of Production Inputs

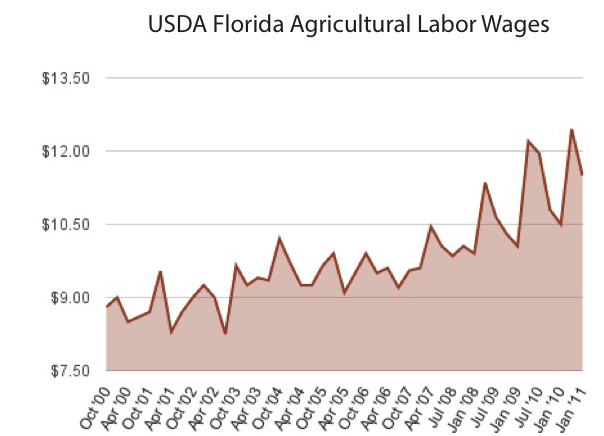

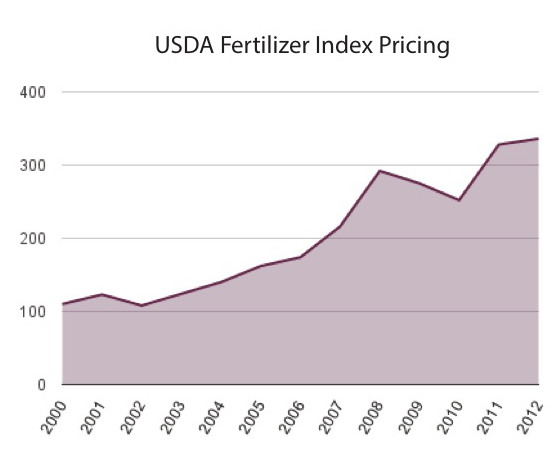

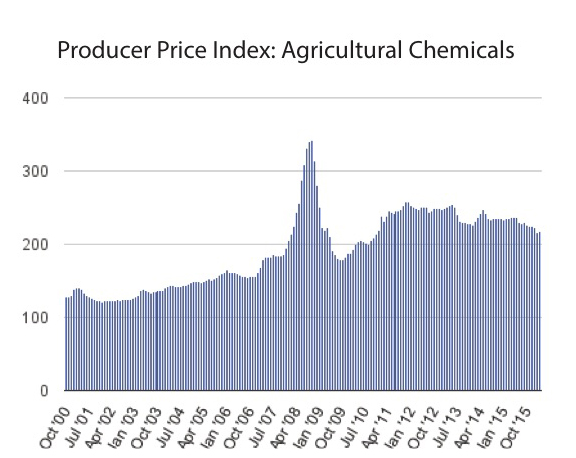

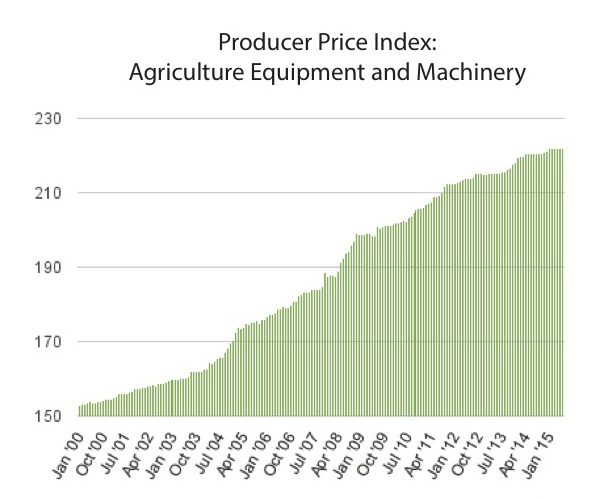

Another way to consider the impact of inflation on tree production is to look at input costs such as agriculture labor wages, fertilizer costs, agricultural equipment and machinery costs, and agricultural chemical costs. The following charts track the nominal price evolution of these inputs since 2000.

These charts help to illustrate how the cost of production inputs for growing trees has increased since 2000. Sobering information when we consider that the price of a 30 gallon live oak is 7% lower today than it was in 2007 and 25% lower than it was in 2000 after adjusting for inflation.

USDA National Agricultural Services Florida Agricultural Labor Wages

USDA Economic Research Service

Producer Price Index by Commodity for Chemicals and Allied Products

Producer Price Index by Commodity for Machinery and Equipment

Return on Invested Capital

Over the long term, supply will expand and contract according to the level of capital investment in the industry. High margins will tend to attract new capital investment, enabling expansion in the aggregate supply. Low margins will keep capital on the sideline. As we have seen, high prices alone do not lead to high margins. Prices must increase at a higher rate than production costs and inflation in order for margins to grow.

Over the past 16 years, margins in the tree industry have been reduced in both nominal and real terms. This has been the result of inflation, the steady increase in the cost of production inputs, and the volatility of pricing.

Ultimately, the price of trees will tend to stabilize at a point where producers are able to achieve a return on invested capital that justifies the level of risk they perceive in the industry. If the return on capital is not high enough to satisfy investor expectations, there will be an attrition of producers over time, leading to more shortages and further escalations in the price.

The expectation for return on invested capital is tied to the level of perceived risk. Factors that drive the perception of risk in our industry are the length of time to produce, market volatility, weather uncertainty, pest and disease and the intensity of upfront capital requirements. Not surprisingly, tree production is a relatively high risk industry and therefore, the expectation for return on invested capital is high relative to other investments.

Conclusions

Based on the analysis discussed above, it is my assessment that the returns on invested capital are substantially below the levels required to attract significant new capital to the industry. Consequently, there will not be significant increases in the supply of trees until prices and margins reach higher more sustainable levels.